Time and time again, gold naysayers have gone to great lengths to dispel its value. “You can’t eat gold,” they would say. This was, apparently, proof that gold is not, in fact, money. Now, the same sort of arguments are being leveraged against bitcoin.

“You can’t even hold it,” “it’s too volatile,” “it’s imaginary money…”

Even goldbugs who have seen their favorite asset fall significantly from its 2011 highs are quick to cast their doubts.

(Source)

The truth here is that speculation can rock even the world’s most recognizable form of money. And that’s exactly what happened with bitcoin in late 2017.

But does that mean the game is over? Absolutely not.

Bitcoin is money. And though it is still young, it is reshaping how money is viewed. It is a response to a broken system, and as the perspective of money evolves, it will play a significant role in the future of currency.

To better understand how the perception of money has changed over the years, let’s backtrack a bit.

The Gold Standard

The gold standard was a monetary system which pegged the value of a state-currency to the price of gold.

A country using the gold standard would set a fixed price for gold and buy and sell the asset at that price. That price would then be tied to that nation’s currency. For example, if a country using the gold standard set the price of gold at $1,000 per ounce, that country’s single-unit currency, the dollar, pound, or euro, would be 1/1000th of an ounce of gold.

The appeal here was that by using the gold standard, a society could prevent inflation or deflation, paving the way for a more equal monetary system while promoting fair pay and full employment.

The gold standard also held one other responsibility – it helped individuals hedge against government missteps. As then-President Herbert Hoover famously noted, “We have gold because we cannot trust governments.”

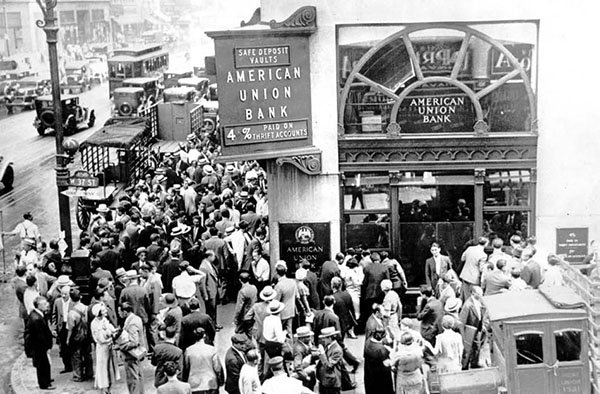

The Emergency Banking Act

Facing economic malaise, Hoover’s predecessor, Roosevelt, set out to revitalize the banking sector.

The initiative began with a nation four-day bank holiday in an attempt to stem bank runs which were bleeding the country’s financial institutions dry. Following the holiday, the Federal Reserve committed to supply unlimited amounts of currency to the country’s banks and created an insurance clause that guarantees the safety of 100 percent of funds deposited.

(Source)

As a result of these new measures, citizens rushed to the reopened banks to re-deposit over half of the funds that were previously removed, and the stock market flourished, gaining 15 percent on the first day of trading after the act was initiated.

But Roosevelt wasn’t finished…

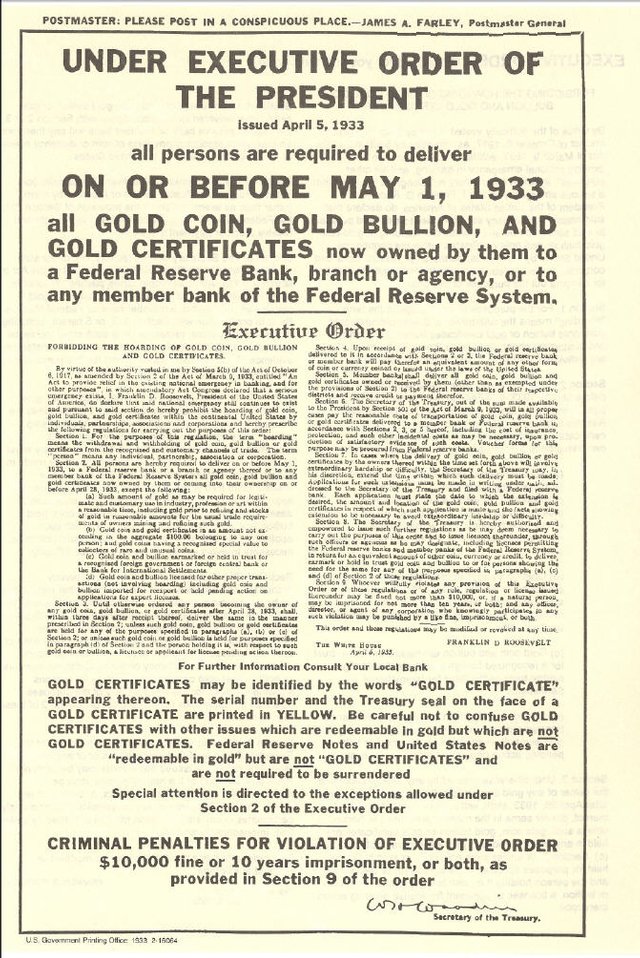

Executive Order 6102

A month later, President Roosevelt signed Executive Order 6102 which criminalized the “hoarding of gold within the United States.”

(Source)

{kind=link}

“The free circulation of gold coins is unnecessary,” President Franklin Roosevelt told Congress, insisting that the transfer of gold “is essential only for the payment of international trade balances.”

The order allowed citizens to redeem their holdings for $20.67 per ounce until May 1, 1933, after which, any possession of gold, minus a few exceptions, would be punishable by law. Several months later, the Roosevelt administration increased the price of the precious metal to $35 per ounce, where it remained until 1971 when the last trace of the Gold Standard was wiped out by Nixon.

During these years, the U.S. dollar became the world’s reserve currency.

Possession of gold remained illegal until 1974 and in 1976, the U.S. monetary system officially transitioned into fiat money.

In the years following, gold prices soared, as did U.S. credit debt and inflation of the U.S. dollar.

The Fall of Physical Cash

Though credit cards and bank cards existed well before the fall of the Gold Standard, it wasn’t until the 1980s and 1990s when the use of plastic began to accelerate.

In 1990, debit cards were used in 300 million transactions, and at that point, banks were still charging hefty fees to both the user and merchants. From maintenance fees and overdraft fees, to fees on merchants every time a card was swiped.

As the use of cards reached modern standards, fees collected by banks skyrocketed. Despite the fees, however, the convenience of plastic ruled the day.

(Source)

The rise of plastic, and the fees associated with it, also ushered in other forms of payment as consumers’ view of money evolved, including digital wallets such as PayPal, Apple Pay, Google Pay, Square and more.

In addition to digital wallets, the world saw a brand-new monetary system arise from the ashes of the 2008 financial collapse – bitcoin.

The Future of Money

Money as we know it today is already digital. We don’t think about physical dollars in our bank accounts when we swipe a card, we think about the numbers on our banking app. Dollars, pounds or euros that may or may not even exist. Money that’s not backed by anything but our trust in the issuer.

Bitcoin has let us shed that trust. We know that this new money exists, because we can see exactly where it is and where it has been.

Bitcoin functions as a unit of account, a store of value, and a medium of exchange. Additionally, as opposed to fiat currencies, it is deflationary.

Where the true value of the dollar has plummeted since it became detached from gold, bitcoin will continue to rise.

The rogue factor in this new money revolution, however, is speculation. In the age of easy credit and cash with no inherent value, it is no surprise that traders and market makers are looking to bitcoin to boost their fiat holdings.

But that bubble will pop.

Conclusion

Economists are beginning to sound the alarms.

U.S. debt has soared to $21 trillion, and it’s showing no signs of slowing.

The stock market bull run is reaching a tipping point.

Years of reckless spending and growing debt have made the global economy vulnerable.

And once promising emerging economies are already experiencing the repercussions.

Bitcoin provides a real solution to these looming economic challenges. A new form of currency not controlled by any government, it is distributed, with no central point of failure, it ignores national borders, and it is open source.

The dollar used to have value, but as soon as it became untethered, purchasing power fell, wages stagnated, and the wealth gap grew to unmanageable levels. In that time, consumers have grown increasingly desensitized.

But what happens when the house of cards collapses?

Will bitcoin prevail?

Featured image via Pixabay

Originally posted on Crypto Insider : https://cryptoinsider.com/bitcoin-better-gold/

Hi! I am a robot. I just upvoted you! I found similar content that readers might be interested in:

https://cryptoinsider.com/bitcoin-better-gold/

Downvoting a post can decrease pending rewards and make it less visible. Common reasons:

Submit