The rise of DEX is to a certain extent related to Compound’s listing of its own tokens in the form of liquid mining in the first half of 2020, which ignited the gameplay of liquid mining. We can also consider this as the fuse. . Liquid mining has brought huge profits to users, and it has also brought huge user increments and funds to the DeFi world. The early DeFi world was based on DEX. It is not difficult to find that high returns have brought exponential capital growth. Even the overall TVL of DeFi is reaching new highs every day.

DEX is not a new thing, subverting the inherent model of CEX. If you mentioned the exchange as a project party in 2018, then the first thing they thought of was the listing fee. At the same time, in the early era of spot market prevalence, CEX will also stipulate that the transaction volume will not meet the standard and will be delisted. currency. If you are an investor, the first few keywords you think of must also be control, centralized market making, robotics, and KYC. For DEX, such as uniswap, you only need to have an Ethereum account. You don't need to deposit your assets in someone else's pockets and then trade like CEX. Through wallet plug-ins such as MetaMask, you can log in to DEX directly with your account, and you can realize transactions, mining, and market making through interaction with decentralized smart contracts. Of course, you also have to pay for the GAS fees generated.

Uniswap is highly open. As a project party, you can also create a fund pool and let your community users come to trade through operations. In this process, no one will charge you for listing fees. Starting from the prevalence of liquid mining in 2020, the 1.0 form of DEX in the DEX world has also been born, represented by Uniswap, SushiSwap, etc., and most of them follow the automatic market maker AMM model. The depth of the transaction is guaranteed by encouraging users to become market makers. Generally speaking, two different currencies of the same value are put into the corresponding liquidity pool. You can obtain corresponding incentives through this method of providing liquidity to the pool, and the more users become automatic market makers, The better the trading depth of the fund pool. But traders have to endure high slippage losses, and automatic market makers have to endure unpaid losses. And any user who has used Uniswap may see a reminder about the unpopular currency, to the effect that this currency may face the risk of not being sold after you buy it. For the 1.0 version of DEX, there is also a huge risk for unpopular small currencies because they do not have enough depth.

1.0 DEX, because there is no order book and no one provides the corresponding external data for it, it is difficult to trade derivatives such as Uniswap at present, even if Uniswap is about to open the V3.0 version, this issue is still open for discussion.

SofaSwap

The 1.0 DEX is still active in the market, but the immutable gameplay is also destined to be relatively limited. The 2.0 DEX is to continuously solve the problems currently facing the DEX world, such as SofaSwap.

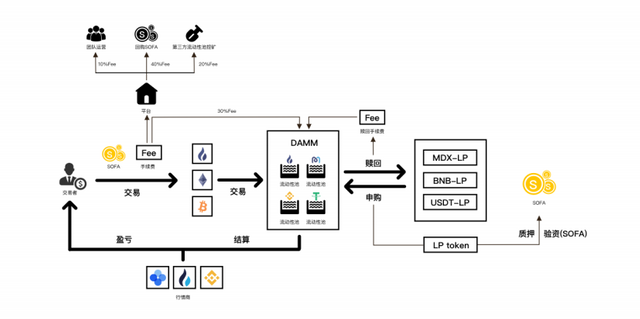

SofaSwap is a new type of DEX, and its positioning is in the derivatives sector. Unlike Uniswap and other AMM (Automated Market Maker) models, SofaSwap uses DAMM (Dynamic Automated Maket Maker) as the technical model of DEX. The DAMM protocol supports Multi Asset Deposit (arbitrary asset mortgage), Free Leverage (free leveraged trading), LiquidityPool (free creation of liquidity pool), Smart Keeper (smart node risk control and settlement), etc., especially any asset mortgage function will be given to DEX model.

In AMM, whether it is a constant product market maker, a constant sum market maker or a constant average market maker, they control the relationship between price and quantity according to a fixed algorithm to maintain the stability of the DEX. This is also a slippage and temporary The root causes of sexual losses, multi-token exposure, and low capital efficiency are also problems that many current AMM-type DEXs have to face. SofaSwap's DAMM model is based on external quotation (accurate and stable), constant fee and formula, dynamic fee and other characteristics to improve the shortcomings of the AMM model, and based on this, makes SofaSwap a cross-currency market financial derivative Transaction agreement. At the same time, SofaSwap is based on DAMM, which is a single currency pledged liquidity market-making system, with very low impermanence losses and relatively low slippage for traders.

Any Asset Mortgage of SofaSwap

Derivatives trading on SofaSwap

First of all, in the DAMM agreement, users trade long or short the price of the target asset. At the same time, they need to pledge the margin to the mortgage pool, and deliver them in the same currency as the margin during settlement. The currency of incoming and outgoing funds (the currency of the payment of the deposit, the currency of the settlement and delivery, and the currency of the fund pool) are the same, but they can be different from the underlying asset currency of the contract. Trading users' buying and selling and mortgages are all completed in the smart contract on the chain, and the liquidity provided by the market maker and redemption liquidity is also completed in the smart contract on the chain. Since then, the overall model is no different from traditional derivatives trading.

After the user puts in the initial margin, sets the leverage and stop-loss to open a long or short position, SofaSwap will package the data on the chain and broadcast it with a timestamp, and then record it on the smart contract. SofaSwap's DAMM agreement will comprehensively weight the prices of the three HBO platforms to obtain a benchmark price, and users will complete long or short transactions at the benchmark price. In the subsequent positions, you can increase the margin or close the profit and stop loss at any time, so as to avoid the risk control system monitoring and starting the smart contract to force the risk control to close the position. So in the above process, the innovation of SofaSwap is that the margin currency can be any asset.

Arbitrary asset mortgage

In CEX, if you hold some unpopular currencies, you have to convert them into mainstream currencies or platform-supported currencies for derivative transactions. In this process, you may face the rise of the currency and bring you The loss that comes. On platforms such as Uniswap, holding some small currencies, in addition to holding spot, can participate in liquidity mining. But the premise is that this proportion of liquidity pool must be created on platforms such as Uniswap, and the overall capital utilization rate is very low.

SofaSwap allows any asset to be used as a collateral deposit for derivatives gameplay. When using the Derivatives function of SofaSwap, users do not need to exchange or trade the asset, and can directly put it as a deposit in the mortgage pool as a deposit to increase the utilization rate of funds. , And also avoid the loss caused by selling the currency.

When users mortgage unpopular assets, they can use the real-time exchange rate and the price of the underlying asset to perform book settlements such as SofaSwap leverage, and during settlement, the actual settlement and delivery will be made in the same currency invested. The user will get an LP after the mortgage, and redeem the assets with the LP. SofaSwap's original trading mechanism that separates the entry and exit currency from the market currency is called the cross-currency market transaction of arbitrary asset mortgage. For example, if you hold a currency in your hand, we assume that it is called A. The liquidity of A currency is normal and there is a large room for long-term appreciation, but it is difficult to improve in the short term. Then we can fully pledge A assets on SofaSwap as a margin to the SofaSwap mortgage pool, as a margin for leveraged games such as BTC, ETH, and even LTC, so as to improve the utilization of funds. Of course, the game of derivatives is naturally risky, and it still needs to be controlled appropriately by taking profit and stopping loss.

In the SofaSwap system, there are two interactive smart contracts. One is called Exchange smart contract, which is equivalent to the entry of SofaSwap's smart contract on the chain, which processes the signature instructions received from the user and the signature instructions issued by the exchange backend. The other is called the Fund smart contract. It is a liquidity pool and a mortgage pool. When we use SofaSwap's leveraged gameplay, the margin will be mortgaged to the Fund smart contract. A currency corresponds to a Fund smart contract, which is managed by the Exchange smart contract. Users and transactions The back office does not directly interact with the Fund smart contract.

From the perspective of any asset mortgage function of SofaSwap, as long as the mortgage pool of the corresponding currency exists, it can be mortgaged, and the creation of the Fund smart contract mortgage pool will be established in the form of a community DAO. SofaSwap will support most public chain assets such as Heco, BSC, Ethereum, etc., and the mortgage pools of the same currency on different chains are independent of each other. Users can only choose one chain for a transaction, and the same chain is used for settlement. The mortgage pool will return the same currency. On the whole, SofaSwap can increase the asset utilization rate of a small share of small currencies in the DEX field, allowing small shares of currencies to be better embedded in the DeFi derivatives sector.

Based on any asset mortgage function of SofaSwap, specifically, users can conduct cross-currency market transactions, such as holding ETH, HT, BNB and even some small currencies such as GXC, DBC, etc., and they can be mortgaged to the mortgage pool The contract operation of mainstream currencies such as BTC is carried out without the need to convert GXC, DBC, etc. into BTC, which can avoid the consumption during the transaction and also avoid the losses caused by the rise of these small currencies. In terms of leveraged gameplay, SofaSwap is regulated by the governance committee of the currency's leverage range, and users can set their own leverage within this range, that is, free leverage, which can not only hedge risks but also expand with small amounts. As the volume of the DeFi world continues to take shape, DEX has gradually evolved and developed. DEX will also be better than CEX in terms of function and experience, and the blue is better than the blue. SofaSwap will also open the blue ocean in the 2.0DEX era.

The meaning of SofaSwapFinally, the significance of SofaSwap is to lower the barriers to entry for the DEX world's derivatives gameplay, and at the same time increase the utilization of funds for various assets, even non-performing assets. SofaSwap's arbitrary asset mortgage function will not be limited to homogenized assets in the future, and it is also expected to introduce NFT. In the long run, with future asset confirmation and NFT certification, SofaSwap's mortgage model will also increase the utilization rate of physical assets in the traditional world, and SofaSwap is also expected to create a broader financial ecosystem.

Follow us:

Twitter: SofaSwap Official

Medium: SofaSwap Official

https://sofaswapofficial.medium.com/

Facebook: SofaSwap Official

https://www.facebook.com/SofaSwapOfficial

Reddit: SofaSwapOfficial