For most Australians, a home loan is the biggest financial commitment we will ever make. It's a credit contract that can last more than 30 years. Most of us have a pretty good idea what interest rate the bank is charging on our mortgage. We wanted to have a streetonomic look at home loan interest, to explain how it is calculated.

In Australia, interest on home loans is quoted as an annual rate, then calculated daily, and charged monthly. The amount you are charged each month depends on your annual interest rate, your daily loan balance and the number of days in the month. Your loan will accrue interest every day. The daily interest accrued is calculated by multiplying your balance by the interest rate, then dividing this by 365. Once a month you are charged interest based on the total of all the daily calculations for that month.

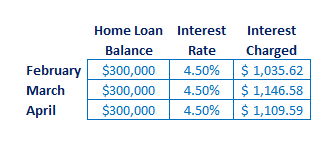

Imagine Mr. Borrower, owes $300,000 on his mortgage and his interest rate is 4.50%. Every day he would accrue interest of around $36.99. If he decides to only make interest only payments, then the interest he would be charged would vary slightly from month to month, depending on how many days are in that month. This is illustrated in the table below:

As we can see, even though the loan balance remains constant at $300,000, his interest charged varies depending on how many days are in the month. Mr. Borrower accrues interest of $36.99 per day on his mortgage. At the end of each month the total of the accrued interest is charged as his monthly interest.

What If Mr. Borrower Made Principal And Interest Payments?

If Mr. Borrower decided to pay off his home loan in 30 years, then his monthly payment would be $1,520 (at an interest rate of 4.50%). His payment can remain constant, but the amount of principal and interest charged each month will vary, as shown below:

Mr. Borrower is makes the same monthly payment to his mortgage. Each month the interest he is charged, and the principal he repays differs slightly. This is due to both the number of days in the month and the home loan balance changing from month to month. When Mr. Borrower first took out his mortgage in February, he was accruing interest at a rate of $36.99 per day. In April his mortgage was accruing interest at $36.88 per day.

The interest rate has remained constant at 4.50%, but the daily interest charged has reduced by 11 cents. This is because Mr. Borrower has reduced his home loan balance by $860, to $299,140. Each month part of his mortgage payment will go toward reducing the principal amount owed. In May his loan will accrue interest at a rate of $36.82 per day.

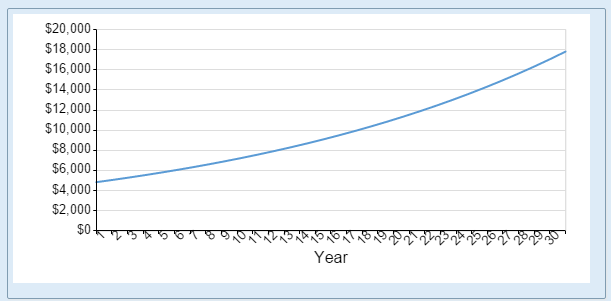

This pattern will continue for the life of the mortgage. Each payment will reduce the rate at which interest is accrued. This in turn means that each payment pays off a little more principal. Over time this will accelerate and the home loan will reduce at an increasing rate. This is due to the effect of compound interest. The chart below shows how much principal Mr. Borrower would repay in each year of his mortgage:

As we can see, in the first year of his mortgage, Mr. Borrower reduces his debt by less than $5,000. By year 30, he will reduce his loan by almost $18,000. This illustrates the effect of compound interest on loan repayments. If Mr.Borrower wanted to accelerate his repayments even further, then he might consider making extra mortgage repayments. Making extra repayments will reduce your loan balance, and save you interest for the remaining life of your mortgage.

What If Mr. Borrower Made Weekly Payments?

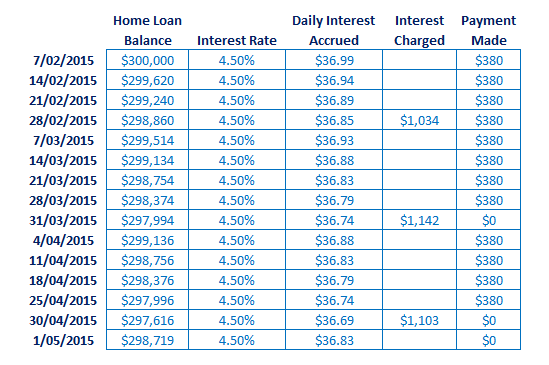

If Mr. Borrower decided to pay 1/4 of his monthly payment every week, then he'd have a weekly payment of $380. The cash flows of making weekly payments over the same 3 months is shown below:

In both the monthly and weekly scenario Mr Borrower has made total repayments of $4,560. On May 1st his mortgage balance will be $298,719 if he makes weekly repayments, and $298,727 if he made monthly payments. Using weekly repayments, Mr. Borrower has reduced his principal by an extra $8. This is because each weekly payment reduces his loan balance, and in turn reduces the daily rate at which his mortgage accrues interest. The benefit comes from making early repayments, rather than waiting till the end of the month.